》Check SMM aluminum product quotes, data, and market analysis

》Subscribe to view historical prices of SMM metal spot cargo

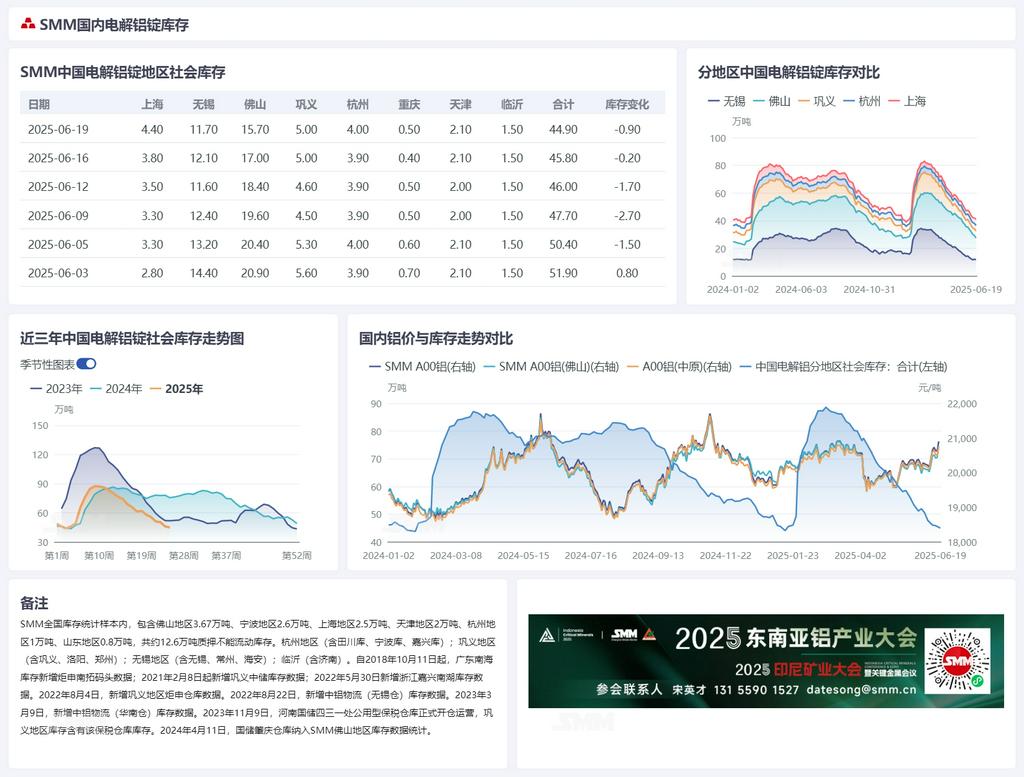

According to SMM statistics, as of June 19, the inventory of primary aluminum ingots in major domestic consumption areas was 449,000 mt, a decrease of 9,000 mt from Monday this week and a decrease of 11,000 mt from Thursday last week.On a YoY basis, it decreased by 307,000 mt compared to the same period last year and by 69,000 mt compared to the same period in 2023, remaining at a low level compared to the same period in the past three years and just shy of the year's low inventory level of 440,000 mt. The supportive effect of low inventory on aluminum prices remains strong.

SMM recently conducted a series of surveys on inter-regional transportation and inventory levels in major domestic consumption areas, summarized as follows:By mid-June, the overall destocking of aluminum ingots in China slowed down this week. At the beginning of the week, influenced by inter-regional transportation driven by regional price spreads and concentrated arrivals over the weekend, there was a significant increase in arrivals in east China's Shanghai, Wuxi, and central China's Gongyi areas over the weekend. Additionally, downstream consumption in the Gongyi area was suppressed by high aluminum prices, affecting outflows from warehouses, making short-term inventory buildup inevitable. Meanwhile, inventory in south China's Foshan area dropped sharply, while inventory in other domestic regions remained largely stable. By mid-week, according to SMM, although inter-regional transportation remained active in the Foshan area due to price spread arbitrage, driving destocking, the recent slight narrowing of the Shanghai-Guangdong price spread and the expectation of further narrowing made it difficult to cover the truck transportation costs between the two regions, reducing the instances of direct transfer of cargo from Foshan to Wuxi warehouses after outflows. Recently, more cargo was transported directly by truck to downstream areas in other parts of east China, particularly areas south of Wuxi (such as Ningbo and Nanchang, where shipping from Wuxi social inventory also incurs certain costs, and recent direct truck transportation costs from Foshan social inventory are more favorable), enabling inventory in the Wuxi area to resume destocking. It is worth noting that the Shanghai area has experienced continuous and significant inventory buildup over the past week due to concentrated arrivals of imported cargo. In the Gongyi area, it is understood that arrivals from the north-west China and other regions have been generally normal recently, with no significant increase observed. Additionally, after spot premiums pulled back mid-week, downstream cargo pick-up increased, and inventory levels remained stable mid-week. Inventory levels in other regions also remained largely stable.

SMM believes that the proportion of liquid aluminum in China is still expected to increase slightly in June, and with the overall domestic casting ingot volume remaining low in the short term, inventory is expected to continue its destocking trend.However, due to the expectation of a slight increase in casting ingot production at a small number of aluminum smelters, recent signs of a slight increase in supply and shipments from the north-west China, as well as inter-regional transportation driven by price spreads, the increase in arrivals this week has already placed significant pressure on east China, potentially alleviating the tight supply of spot cargo in the market to some extent. Looking ahead, aluminum prices have been holding up well at high levels recently, which will inevitably have a certain inhibitory effect on domestic demand during the off-season. There is an expectation of weaker outflows from warehouses, which will put pressure on the slowdown of overall domestic destocking in the second half of the month. Close attention should be paid to whether the annual low of 440,000 mt can be successfully refreshed before the signal of a shift from the off-season to inventory buildup becomes clear (for the time being, SMM suggests focusing on the key time point from late June to early July), in order to determine the next direction of market sentiment.